[ad_1]

Source: The Hindu

- Prelims: Indian Economy(Fiscal Policy, GST)

- Mains GS Paper III: Fiscal policy, GST Council, Cooperative Federalism etc

ARTICLE HIGHLIGHTS

- In 2018, the late FinanceMinister, announced that the 28% GST slab, which he called the “dying slab”, would be phased out, except for luxury items.

- India, he said, would eventually have just two slabs: 5% and a standard rate between 12% and 18% (apart from exempt items).

Puucho ON THE ISSUE

Context

Goods and Services Tax(GST)

- GST was introduced through the 101st Constitution Amendment Act, 2016.

- It is the biggest indirect tax reform in the country.

- It was introduced on the pretext of ‘One Nation One Tax’.

- It has subsumed indirect taxes like excise duty, Value Added Tax (VAT), service tax, luxury tax

- It is levied at the final consumption point and is essentially a consumption tax.

- It has led to a common national market as it helped mitigate the double taxation, cascading effect of taxes, multiplicity of taxes, classification issues etc.

- The GST paid by a merchant to procure goods or services (i.e. on inputs) can be set off later against the tax applicable on supply of final goods and services.

- The GST avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

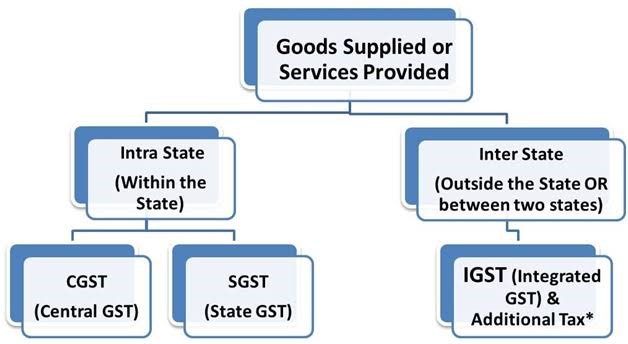

Tax Structure under GST:

- Central GST to cover Excise duty, Service tax etc

- State GST to cover VAT, luxury tax

- Integrated GST (IGST) to cover inter-state trade. It is not a tax per se but a system to coordinate state and union taxes.

- It has a 4-tier tax structure for all goods and services under the slabs- 5%, 12%, 18% and 28%.

Issues with GST:

- Imposing a high GST in some areas does not make sense.

- ‘Sin’ taxes, for instance, are at cross purposes with the government’s policy of generating growth and creating jobs under Make in India’.

- The hotel generates indirect employment in ancillary areas: it buys bed linen, furnishings, rugs and carpets, air conditioners, cutlery, electrical fittings and furniture, and consumes enormous quantities of food produce. All these generate jobs and income for farmers, construction contractors,artisans and other manufacturers.

- Five star hotels also generate foreign exchange by attracting rich tourists and visitors. So, it’s unwise to tax these hotels to death.

- High taxes on air conditioners, air conditioned restaurants, chocolates and luxury cars create an economic ripple effect downstream, in a complex web of businesses that have symbiotic relationships. The effect finally reaches down to the bottom of the employment pyramid.

- GST on bread is zero, but the vegetable sandwich is in the 5% tax slab, hitting the vegetable grower directly.

- Taxes on wine, rum and beer, which generate large-scale employment and are the backbone of grape and sugarcane farming and the cocoa industry.

- In the automobile sector, the GST on electric cars, tractors, cycles,bikes, low end and luxury cars ranges anywhere from 5% to 50%. The Sale of automobiles is the barometer of an economy.

- The confusion has given rise to several disputes. ID Fresh Food, for instance, which makes ready to eat foods like chapatis, rotis, parotas and sells various types of idli and dosa batter appealed against a GST ruling of the Authority for Advance Rulings.

- There are items that are exempt from GST. Petrol, diesel, aviation turbine fuel are not under the purview of GST, but come under Central excise and State taxes.

- Central excise duties and varying State Taxes contribute over 50% of the retail price of petrol and diesel, probably the highest in the world barring banana republics.

- There is distrust between the States and the Centre on revenue sharing. There is also anger at the Centre for riding roughshod over the States’ autonomy and disregarding the federal structure of the Constitution.

GST Compensation:

- In theory the GST should generate as much revenue as the previous tax regime.

- The new tax regime is taxed on consumption and not manufacturing.

- The tax won’t be levied at the place of production which also means manufacturing states would lose out and hence several states strongly opposed the idea of GST.

- It was to assuage these states that the idea of compensation was mooted.

- The Center promised compensation to the States for any shortfall in tax revenue due to GST implementation for a period of five years.

- This promise convinced a large number of reluctant States to sign on to the new indirect tax regime.

Compensation Cess:

- Under the GST (Compensation to States) Act, 2017, the percentage of annual revenue growth of a State has been projected to be 14%.

- If the annual revenue growth of a State is less than 14%, the State is entitled to receive compensation under the statute.

- The compensation payable to a State shall be provisionally calculated and released at the end of every two months period.

- States are guaranteed compensation for any revenue shortfall below 14% growth (base year 2015-16) for the first five years ending 2022.

- All the taxpayers, except those who export specific notified goods and those who have opted for GST composition scheme, are liable to collect and remit the GST compensation cess to the central government.

GST Compensation Cess consists of:

- Cess levied on sin and luxury goods for five years.

- The entire cess collected during the year is required to be credited to a non-lapsable Fund (the GST Compensation Cess Fund).

- The collected compensation cess flows into the CFI and is then transferred to the Public Account of India, where the GST compensation cess fund has been created.

Federalism:

- Federalism in essence is a dual government system including the Centre and a number of States. Federalism is one of the pillars of the Basic Structure of the Constitution.

- R. Bommai vs Union of India case, the States are not mere appendages of the Union and the latter should ensure that the powers of the States are not trampled with.

Supreme Court on Federalism:

- Federalism in India is “a dialogue in which the states and the Centre constantly engage in conversations”.

- It is not imperative that one of the federal units (Centre or states) must always possess a higher share of power over the other units.

- It said that recommendations of the GST Council “are the product of a collaborative dialogue involving the Union and States”.

- It pointed out that Article 246A of the Constitution stipulates that both Parliament and state legislatures have “simultaneous” power to legislate on GST.

Cooperative Federalism:

- It is a horizontal relationship between centre and state, where they “cooperate” in the larger public interest.

- It enables states’ participation in the formulation and implementation of national policies.

- Both centre and State are constitutionally obliged to cooperate with each other on the matters specified in Schedule VII of the constitution.

Competitive Federalism:

- The relationship between the Central and state governments is vertical and between state governments is horizontal.

- The endowments of states in the free-market economy, available resource base and their comparative advantages all foster a spirit of competition.

- In Competitive federalism States compete among themselves and also with the Centre for benefits.

- It is not part of the basic structure of the Indian constitution. It is the decision of the executives.

- States compete with each other to attract funds and investment, which facilitates efficiency in administration and enhances developmental activities.

| KISS principle:

● It is an acronym for keep it simple, stupid, is a design principle noted by the U.S. Navy in 1960. ● The KISS principle states that most systems work best if they are kept simple rather than made complicated; therefore, simplicity should be a key goal in design, and unnecessary complexity should be avoided. ● The low cost airline model is successful because of the KISS principle. All The frills such as food, freebies and assigned seats are dispensed with.

Article 246A: Parliament and the Legislature of every State, have power to make laws with respect to goods and services tax imposed by the Union or by such State.

Article 279A:The President shall, within sixty days from the date of commencement of the Constitution (One Hundred and First Amendment) Act, 2016, by order, constitute a Council to be called the Goods and Services Tax Council.

Cascading effect of tax: when there is a tax levied on a product at every step of sale. The tax is levied on a value that includes tax paid by previous buyers thus making end consumer pay tax on already paid tax.

|

Way Forward

- The directives to the bureaucracy is necessary from the ruling dispensation to come up with just two categories: goods eligible for zero tax and goods that will fall under a single rate, say 10% or 12%, everything except those specifically exempt, is taxed.

- The plan must be to figure out how to rev up the economy by making the rich and upper middle class spend and move more people up the value chain in order that more chocolates and ACs and automobiles are bought by them, instead of designing a tax system that keeps these products out of the new consumer class’s reach.

- The government should do away with all the confusing tax slabs in one fell swoop. It can usher in a truly single low tax regime along with a list of exempt items. That will ensure compliance, widen the tax net, improve ease of doing business, boost the economy, create jobs, increase tax collections and reduce corruption as witnessed in many countries –a move that will be both populist and well regarded by economists.

- GST is a positive step towards shifting the Indian economy from the informal to formal economy. It is important to utilize experiences from global economies that have implemented GST before us,to overcome the impending challenges.

QUESTION FOR PRACTICE

India should follow a unified single tax regime as empirical data from across the world on the benefits of a unified single tax is incontrovertible. Do you agree with this statement? Justify your answer with proper arguments.

(200 WORDS, 10 MARKS)

[ad_2]