[ad_1]

Context:

Recently, India’s central bank released several key documents that further shed light on the challenges faced by the Indian economy as well as the RBI (as the authority regulating the monetary policy of the country).

Many recall the key dilemma facing the RBI in the recent past has been the sharp trade-off between economic growth and inflation.

That’s because, since November 2019, India’s inflation rate has been persistently high and economic growth rate persistently low.

However, between supporting growth and containing inflation — the two require diametrically opposite policy responses the RBI has repeatedly favoured the former.

This is a choice that pre-dates the Covid-induced disruption.

Challenges faced by the RBI:

- The economic disruption caused by the Covid-19 pandemic has brought growth concerns to the top of Indian monetary policy makers’ priority list, and relegated the inflation goal to a secondary position.

- In the wake of global anthropological shock Covid-19, a sharp slowdown in economic growth and employment prospects is evident in the Indian economy.

- In this context, Reserve Bank of India’s role in ensuring economic stability, growth and development through effective monetary policy assumes more importance than ever.

- RBI’s job involves balancing short-term as well as long-term growth, ensuring economic growth while meeting the inflation targets.

- However, issues pertaining to the incomplete transmission of monetary policy and inherent weakness of inflation targeting approach, are some of the challenges faced by RBI.

Easy Money policy today could lead to high interest rates in the economy tomorrow:

- Easy money is when the RBI allows cash to build up within the banking system—as this lowers interest rates and makes it easier for banks and lenders to loan money.

- Easy money is a representation of how the RBI can stimulate the economy using monetary policy.

- The central bank looks to create easy money when it wants to lower unemployment and boost economic growth, but a major side effect of doing so is inflation.

- When money is easy (i.e., cheaper) to borrow, it can stimulate spending, investment, and economic growth.

- If easy money persists for too long, however, it can lead to high inflation.

- Too much easy money can cause the economy to overheat. It can incentivize over-investment in projects with poor outlooks. Discourages saving since interest rates on deposit accounts are low.

Ill-effects of rising Inflation over a period of time:

Inflation encourages current consumption (buy goods and services now before prices rise) and discourages savings.

- People with savings suffer in times of inflation as the purchasing power of their savings decreases as price levels rise.

- The real rate of interest (nominal rate less the inflation rate) is reduced in times of inflation.

- Real interest rates may be negative if inflation rate is greater than the interest rate. If so the purchasing power of savings declines. This discourages savings.

- People who have borrowed money benefit as the real value of loans decreases as price levels rise (loans are easier to repay in the future as prices and income rise over time).

Borrowers benefit as inflation reduces the real value (the purchasing power) of the money they owe.

People who have borrowed money benefit as the real value of loans decreases as price levels rise (loans are easier to repay in the future as prices and income rise over time).

- Inflation, the steady rise of prices for goods and services over a period, has many effects, good and bad.

- Inflation erodes purchasing power or how much of something can be purchased with currency.

- Because inflation erodes the value of cash, it encourages consumers to spend and stock up on items that are slower to lose value.

- It lowers the cost of borrowing and reduces unemployment.

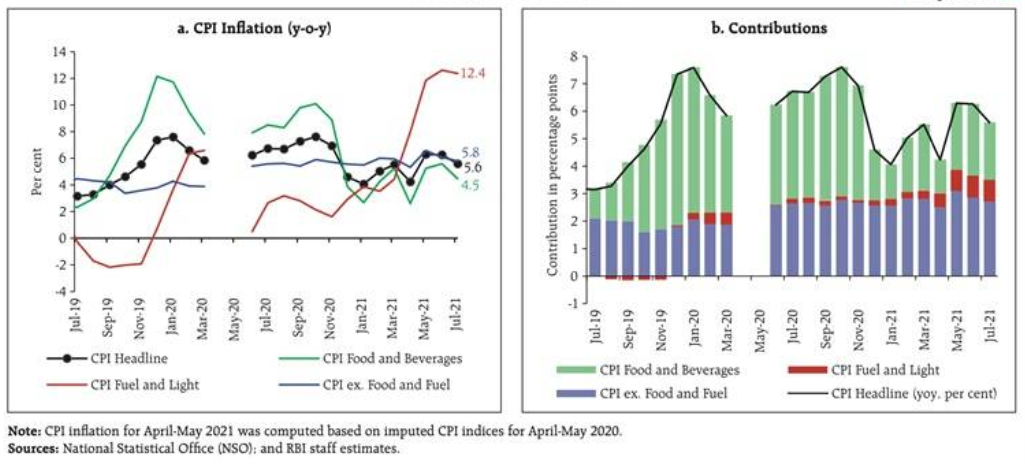

However, recent review by RBI Monetary Policy Committee:

- Inflationary pressures are being closely and continuously monitored. The MPC is conscious of its objective of anchoring inflation expectations.

- The outlook for aggregate demand is improving, but still weak and overcast by the pandemic. There is a large amount of slack in the economy, with output below its pre-pandemic level.

- The current assessment is that the inflationary pressures during Q1:2021-22 are largely driven by adverse supply shocks which are expected to be transitory.

- While the Government has taken certain steps to ease supply constraints, concerted efforts in this direction are necessary to restore supply-demand balance.

- The nascent and hesitant recovery needs to be nurtured through fiscal, monetary and sectoral policy levers.

- Accordingly, the MPC decided to keep the policy repo rate unchanged at 4 per cent and continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

Conclusion:

Domestic economic activity is starting to recover with the ebbing of the second wave.

Looking ahead, agricultural production and rural demand are expected to remain resilient.

Urban demand is likely to mend with a lag as manufacturing and non-contact intensive services resume on a stronger pace, and the release of pent-up demand acquires a durable character with an accelerated pace of vaccination.

Buoyant exports, the expected pick-up in government expenditure, including capital expenditure, and the recent economic package announced by the Government will provide further impetus to aggregate demand.

Although investment demand is still anaemic, improving capacity utilisation and congenial monetary and financial conditions are preparing the ground for a long-awaited revival.

[ad_2]