[ad_1]

Context:

Taking the first step towards having a digital currency in the country, Prime Minister Narendra Modi launched an electronic voucher based digital payment system “e-RUPI”.

The platform, which has been developed by the National Payments Corporation of India (NPCI), Department of Financial Services, Ministry of Health and Family Welfare and the National Health Authority, will be a person-specific and purpose-specific payments system.

Capturing the unbanked and helping underprivileged:

- With a population of 1.3 billion, India is the world’s second-most populous country and the world’s seventh-largest at 3.288 million sq km.

- Although the nation has achieved grain self-sufficiency from its largest industry, agriculture, production remains resource-intensive, cereal-centric, and regionally biased.

- Food security is still an issue for the majority of people, and the poverty rate is still high at 30%.

- This initiative seems like one of the ways the government is trying to digitalize, while at the same time provide opportunities and resources for the underprivileged.

- According to local reports, government embarked on this to capture the unbanked population, who mostly comprise the

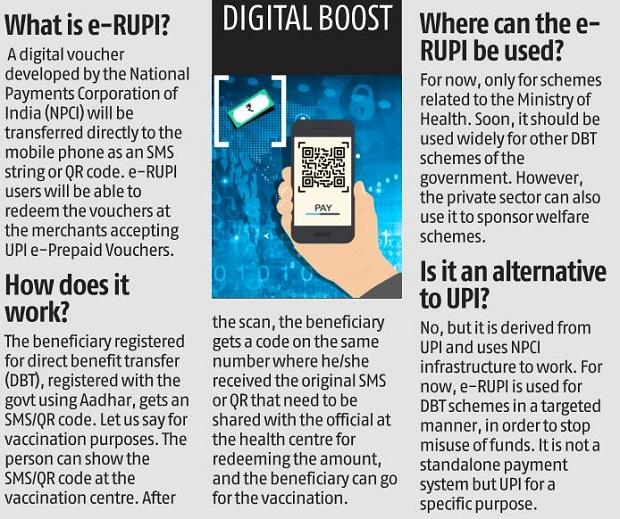

How will e-RUPI work?

e-RUPI is a cashless and contactless digital payments medium, which will be delivered to mobile phones of beneficiaries in form of an SMS-string or a QR code.

This will essentially be like a prepaid gift-voucher that will be redeemable at specific accepting centres without any credit or debit card, a mobile app or internet banking.

e-RUPI will connect the sponsors of the services with the beneficiaries and service providers in a digital manner without any physical interface.

It is important to note, however, that e-RUPI is neither a cryptocurrency nor a central bank digital currency (CBDC). It is also not a digital or e-wallet either, which may admittedly sound strange to some.

Does India have appetite for a digital currency?

According to the RBI, there are at least four reasons why digital currencies are expected to do well in India:

- One, there is increasing penetration of digital payments in the country that exists alongside sustained interest in cash usage, especially for small value transactions.

- Two, India’s high currency to GDP ratio, according to the RBI, “holds out another benefit of CBDCs”.

- Three, the spread of private virtual currencies such as Bitcoin and Ethereum may be yet another reason why CBDCs become important from the point of view of the central bank.

- As Christine Lagarde, President of the ECB has mentioned in the BIS Annual Report “central banks have a duty to safeguard people’s trust in our money. Central banks must complement their domestic efforts with close cooperation to guide the exploration of central bank digital currencies to identify reliable principles and encourage innovation.”

- Four, central bank digital currency (CBDC) might also cushion the general public in an environment of volatile private VCs.

Global examples of a voucher-based welfare system:

In the US, there is the system of education vouchers or school vouchers, which is a certificate of government funding for students selected for state-funded education to create a targeted delivery system.

These are essentially subsidies given directly to parents of students for the specific purpose of educating their children.

In addition to the US, the school voucher system has been used in several other countries such as Colombia, Chile, Sweden, Hong Kong, etc.

How will these vouchers be issued?

The system has been built by NPCI on its UPI platform, and has onboarded banks that will be the issuing entities.

Any corporate or government agency will have to approach the partner banks, which are both private and public-sector lenders, with the details of specific persons and the purpose for which payments have to be made.

The beneficiaries will be identified using their mobile number and a voucher allocated by a bank to the service provider in the name of a given person would only be delivered to that person.

Significance of e-RUPI and how is it different than a digital currency:

- The government is already working on developing a central bank digital currency and the launch of e-RUPI could potentially highlight the gaps in digital payments infrastructure that will be necessary for the success of the future digital currency.

- In effect, e-RUPI is still backed by the existing Indian rupee as the underlying asset and specificity of its purpose makes it different to a virtual currency and puts it closer to a voucher-based payment system.

- Also, the ubiquitousness of e-RUPI in the future will depend on the end-use cases.

- Even the private sector can leverage these digital vouchers as part of their employee welfare and corporate social responsibility programs.

Conclusion:

According to government, e-RUPI is easy, safe and secure as it keeps the details of the beneficiaries completely confidential.

The entire transaction process through this voucher is relatively faster and at the same time reliable, as the required amount is already stored in the voucher.

e-RUPI is expected to ensure a leak-proof delivery of welfare services. It can also be used for delivering services under schemes meant for providing drugs and nutritional support under Mother and Child welfare schemes, TB eradication programmes, drugs & diagnostics under schemes like Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, fertiliser subsidies etc.

The government also said that even the private sector can leverage these digital vouchers as part of their employee welfare and corporate social responsibility programmes.

It also guarantees that the service provider is only paid once the transaction has been completed.

[ad_2]