[ad_1]

Introduction:

Cryptocurrency will be discouraged via taxation and capital gains provisions.

Ukraine has been a centre for cryptos trading due to its lax rules and is using them to raise funds for its war with Russia.

The Governor of the Reserve Bank of India highlighted two things:

First, “private cryptocurrencies are a big threat to our financial and macroeconomic stability”.

Second, “these cryptocurrencies have no underlying (asset)… not even a tulip”.

Soon thereafter, a Deputy Governor of the RBI called cryptos worse than a Ponzi scheme and argued against “legitimizing” them.

Yet, the RBI announced that it will float a Central Bank Digital Currency (CBDC).

Concept of “Central Bank Digital Currency (CBDC)” and its impact on the banking system:

- CBDC is the same as currency issued by a central bank but takes a different form than paper.

- It is the sovereign currency in an electronic form and it would appear as a liability (currency in circulation) on a central bank’s balance sheet.

- The underlying technology, form, and use of a CBDC can be molded for specific requirements. CBDCs should be exchangeable at par with cash.

- While interest in CBDCs is universal now, very few countries have reached even the pilot stage of launching their CBDCs.

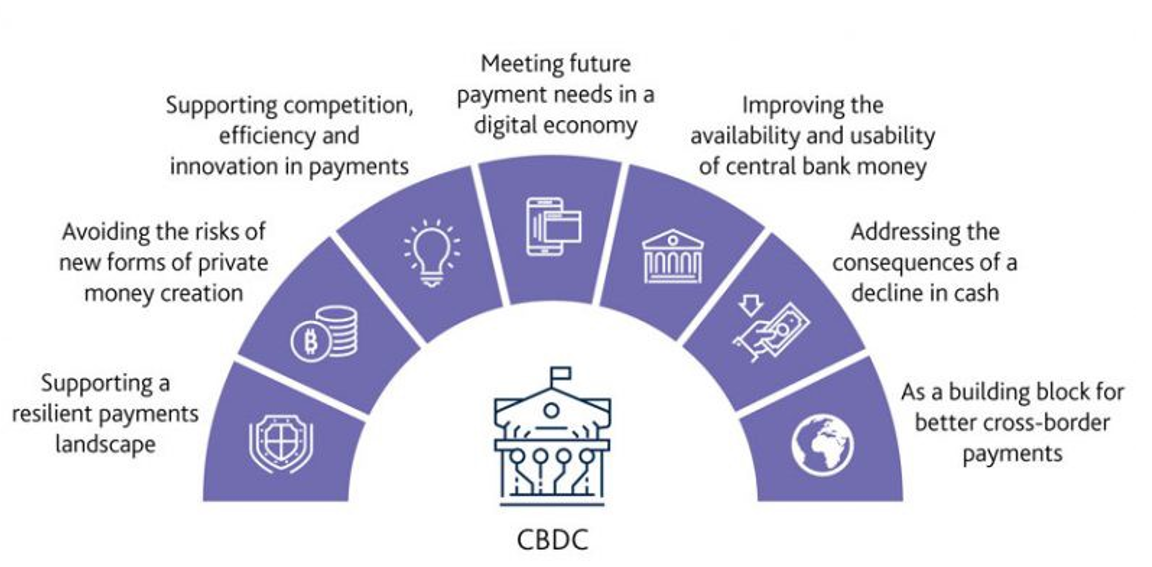

Adoption of CBDC has been justified for the following reasons:-

- Central banks, faced with dwindling usage of paper currency, seek to popularize a more acceptable electronic form of currency (like Sweden).

- Jurisdictions with significant physical cash usage seeking to make issuance more efficient (like Denmark, Germany, or Japan, or even the US).

- Central banks seek to meet the public’s need for digital currencies, manifested in the increasing use of private virtual currencies, and thereby avoid the more damaging consequences of such private currencies.

- The CBDC has many advantages to offer like reduced cost, and better central control over the paper currency.

- The present banking system needs to be part of the CBDC Pilot projects in the Indian context.

- The acceptance and anonymity of paper currency can be attained with CBDC only with time and gradual acceptance.

Need of CBDC:

CBDC will be backed by distributed ledger technology (DLT) but will be a permissioned blockchain which will make it different from other permissionless crypto assets.

The central monetary authority will have control access to the blockchain. Central banks are facing dwindling usage of paper currency and now seek to popularize a more acceptable electronic form of currency.

Digital currency will be more efficient and will be able to avoid the damaging consequences of private currencies.

Cryptos as currency:

- A CBDC will not solve the RBI’s problem since it can only be a fiat currency and not a crypto. However, cryptos can function as money. This difference needs to be understood.

- A currency is a token used in market transactions. Historically, commodities (such as copper coins) have been used as tokens since they themselves are valuable.

- But paper currency is useless till the government declares it to be a fiat currency. It is only then that everyone accepts it at the value printed on it.

- So, paper currency derives its value from state backing. Cryptos are a string of numbers in a computer programme and are even more worthless.

- Bitcoin, the most prominent crypto, has been designed to become expensive.

- Its total number is limited to 21 million and progressively requires more and more computer power and energy to produce (called mining, like for gold). As the cost of producing bitcoin has risen, its price has also increased.

- This has led to speculative investment which drives the price higher and attracts more investors. So, since 2009, in spite of wildly fluctuating prices, they have yielded high returns making speculation successful.

CBDC, unlike cryptos:

Blockchain enables decentralisation. That is, everyone on the crypto platform has a say. But central banks would not want that.

Further, they would want a fiat currency to be exclusively issued and controlled by them. But, theoretically everyone can ‘mine’ and create crypto.

So, for the CBDC to be in central control, solving the ‘double spending’ problem and being a crypto (not just a digital version of currency) seems impossible.

A centralized CBDC will require the RBI to validate each transaction — something it does not do presently. Once a currency note is issued, the RBI does not keep track of its use in transactions.

Centralized CBDC:

CBDCs are not going to replace bitcoin or cryptocurrencies unless they are part of a broader state plan to crack down on bitcoin.

The centralized nature of CBDCs will enable more surveillance and further erode financial privacy of individuals in the economy.

One can argue that there are costs to handling cash and coin, from inconvenience to loss of tax revenue, which CBDC’s would resolve.

No matter what circumstances the implementation of CBDC occurs under, Bitcoin will never die, and the community’s ingenuity and creativity will ensure we have a market and economy thriving with Bitcoin as the people’s currency.

Conclusion:

CBDCs at present cannot be a substitute for cryptos that will soon begin to be used as money. This will impact the functioning of central banks and commercial banks.

Further, a ban on cryptos requires global coordination, which seems unlikely.

However, Blockchain and encryption have solved the problem by devising protocols such as ‘proof of work’ and ‘proof of stake’.

They enable the use of cryptos for transactions. While the first protocol is difficult, the second is simpler but prone to hacking and fraud.

Today, thousands of different kinds of cryptos exist; Bitcoin like cryptos, Alt coins and Stable coins.

[ad_2]