[ad_1]

Context:

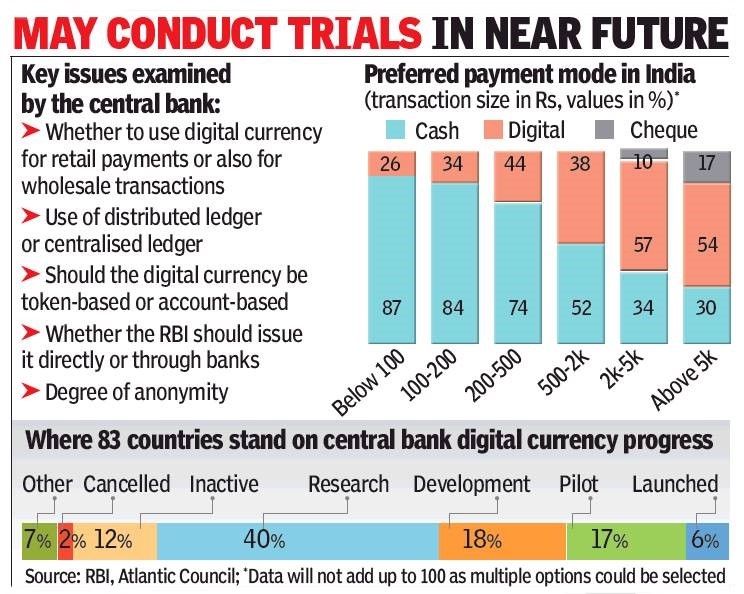

The Reserve Bank of India (RBI) recently said that it has been working towards a phased implementation strategy central bank digital currency (CBDC).

While the move has been welcomed by industry stakeholders, a few statements made by RBI have stoked concerns regarding the future of virtual currencies (VCs) such as bitcoin, ether and dogecoin.

RBI is currently working towards a phased implementation strategy and examining use cases which could be implemented with little or no disruption.

CDBCs are digital currencies issued by a central bank, and generally take on a digital form of the nation’s existing fiat currency such as the rupee.

Viability of Digital Currency:

In contrast to India’s continued ambiguity over the legality of cryptocurrencies, its stance on introducing an official digital currency has been reassuringly clear and consistent over time.

And, four years after an inter-ministerial committee recommended that India launch fiat money in digital form, the Reserve Bank of India has indicated that pilot projects to figure out its viability are likely to be launched soon.

The clarity is welcome, given that the much-awaited Cryptocurrency and Regulation of Official Digital Currency Bill, 2021, is yet to be introduced.

Background of Digital currencies by central banks:

The idea of “Central Bank Digital Currencies” (CBDC) is not a recent development.

Some attribute the origins of CBDCs to Nobel laureate James Tobin2, an American economist, who in 1980s suggested that that Federal Reserve Banks in the United States could make available to the public a widely accessible ‘medium with the convenience of deposits and the safety of currency.’

It is only in the last decade, however, that the concept of digital currency has been widely discussed by central banks, economists & governments.

What is the need for a CBDC?

While interest in CBDCs is near universal now, very few countries have reached even the pilot stage of launching their CBDCs.

- A 2021 BIS survey of central banks found that 86% were actively researching the potential for CBDCs, 60% were experimenting with the technology and 14% were deploying pilot projects.

- The adoption of CBDC has been justified for the following reasons:

- Central banks, faced with dwindling usage of paper currency, seek to popularize a more acceptable electronic form of currency (like Sweden);

- Jurisdictions with significant physical cash usage seeking to make issuance more efficient (like Denmark, Germany, or Japan or even the US);

- Central banks seek to meet the public’s need for digital currencies, manifested in the increasing use of private virtual currencies, and thereby avoid the more damaging consequences of such private currencies.

- In addition, CBDCs have some clear advantages over other digital payments systems, payments using CBDCs are final and thus reduce settlement risk in the financial system.

- Imagine a UPI system where CBDC is transacted instead of bank balances, as if cash is handed over, the need for interbank settlement disappears.

- CBDCs would also potentially enable a more real-time and cost-effective globalization of payment systems.

- It is conceivable for an Indian importer to pay its American exporter on a real time basis in digital Dollars, without the need of an intermediary.

- This transaction would be final, as if cash dollars are handed over, and would not even require that the US Federal Reserve system is open for settlement.

- Time zone difference would no longer matter in currency settlements – there would be no ‘Herstatt’ risk.

Central Bank Digital Currency – Is This the Future of Money:

- A CBDC is the legal tender issued by a central bank in a digital form.

- It is the same as a fiat currency and is exchangeable one-to-one with the fiat currency. Only its form is different.

- CBDC is the same as currency issued by a central bank but takes a different form than paper (or polymer).

- It is sovereign currency in an electronic form and it would appear as liability (currency in circulation) on a central bank’s balance sheet.

- The underlying technology, form and use of a CBDC can be moulded for specific requirements. CBDCs should be exchangeable at par with cash.

- India is leading the world in terms of digital payments innovations. Its payment systems are available 24X7, available to both retail and wholesale customers, they are largely real-time, the cost of transaction is perhaps the lowest in the world.

- There is thus a unique scenario of increasing proliferation of digital payments in the country coupled with sustained interest in cash usage, especially for small value transactions.

- To the extent the preference for cash represents a discomfort for digital modes of payment, CBDC is unlikely to replace such cash usage.

- But preference for cash for its anonymity, for instance, can be redirected to acceptance of CBDC, as long as anonymity is assured.

- India’s high currency to GDP ratio holds out another benefit of CBDCs. To the extent large cash usage can be replaced by CBDCs, the cost of printing, transporting, storing and distributing currency can be reduced.

Conclusion:

Introduction of “Central Bank Digital Currencies” (CBDC) has the potential to provide significant benefits, such as reduced dependency on cash, higher seigniorage due to lower transaction costs, reduced settlement risk.

Introduction of CBDC would possibly lead to a more robust, efficient, trusted, regulated and legal tender-based payments option.

There are associated risks, no doubt, but they need to be carefully evaluated against the potential benefits.

It would be RBI’s endeavour, as we move forward in the direction of India’s CBDC, to take the necessary steps which would reiterate the leadership position of India in payment systems.

CBDCs is likely to be in the arsenal of every central bank going forward. Setting this up will require careful calibration and a nuanced approach in implementation.

Drawing board considerations and stakeholder consultations are important. Technological challenges have their importance as well.

As is said, every idea will have to wait for its time. Perhaps the time for CBDCs is nigh.

[ad_2]